Yew Kee Duck Rice started as a push-cart business in the 1950s. Since then, Executive Chairman Seah Boon Luck, who has taken over from his father, has grown an F&B empire under the name YKGI Limited (“YKGI” or “the Company”) that runs a diverse portfolio of non-Halal and Halal brands. See www.ykgi.com.sg for more information.

The Company runs 1 central kitchen, and 43 food outlets under multiple brands, including Yew Kee Duck Rice (友记鸭饭), XO Minced Meat Noodles, My Kampung Chicken Rice, PastaGo, and Victoria Bakery. The Company manages four food courts and holds the exclusive franchise for all 30 CHICHA San Chen (吃茶三千) bubble tea outlets in Singapore.

On 30 December 2022, the Company lodged its draft prospectus for a Catalist listing on the Singapore Exchange and made its debut on 6 February 2023. Stock Code: SGX: YK9.

Post-IPO, YKGI Limited will build its track record of financial performance over time. But we can take a look at the financial performance of its Catalist-listed peers, and in this way, monitor and compare YKGI’s performance as the months go by. This will give us a sense of what we should expect and thus be able to do a more detailed analysis and valuation of the stock for investment decision-making in the future.

N.M. = Not Meaningful / N/A = Not Available

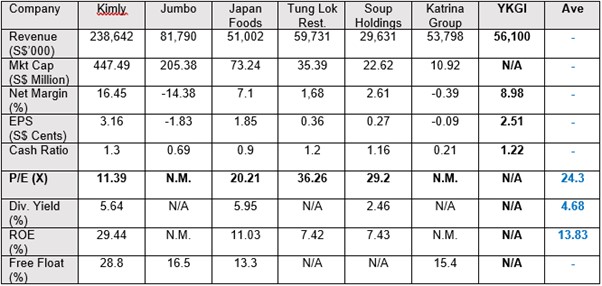

Table 1’s selected financials of YKGI peers attempts to give a rounded picture of each stock.

For example, revenue and market cap pertain to size, net profit margin % and EPS to profitability, cash ratio to liquidity, P/E to valuation, dividend, and ROE to investor returns. But of course, for YKGI, some of these numbers are not yet available as at the date of writing ie 3 February 2023. Even among the listed peers, some of the financials are not available or not meaningful e.g. losses will render P/E Not Meaningful.

However, we can have an indication of what YKGI’s potential or prospects are by searching for the peer with the highest degree of similarity to it. If we take those financials which are ratios, they are inter-comparable. (Revenue is not comparable not only because it is not a ratio, but more importantly, the business of a company usually enjoys significant economies of scale as revenue grows).

The retail F&B business has very significant economies of scale such as in bulk purchasing, fixed costs, and central kitchens, which is why every retail F&B company wants to set up a chain of branches.

Just by looking at YKGIs products and business model, we can see that it bears more similarity to Kimly than to the other peers listed here. Duck rice stalls, food courts, minced meat noodles, and chicken rice. Definitely not Tung Lok shark fin or Jumbo chili crab.

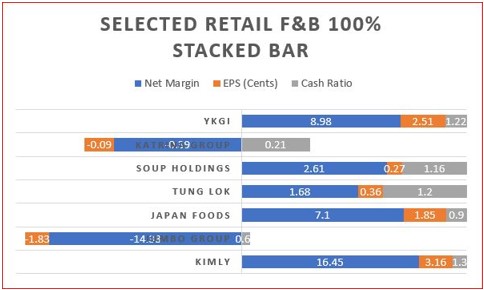

Is this true? We take those financials that are available and comparable for all 6 companies here: Net Profit Margin, EPS, and Cash Ratio. This is not a comprehensive comparison, but it will give you a rough idea of the degree of similarity/dissimilarity between the six companies. After all, cash flow and high net profit margin are two main characteristics of retail F&B that are also prized by investors. It is unfortunate that for our selected period of study FY2021, the Covid-19 pandemic’s mobility restrictions as well as economic impact wreaked havoc on high-end retail F&B like Jumbo and Tung Lok where demand is more elastic.

It is not so painful to forego shark fin and chili crab if you can have duck rice and chicken rice. Even the mid-tier Katrina Group that has to pay high rentals for their mall outlets suffered as economies of scale reversed into diseconomies of scale. As for Japan Foods despite operating as restaurants in malls it has had a long track record of profitability. But the reasons for its resilience can only be discerned with a detailed study of its operations and management.

Chart 1 above shows that the degree of similarity is highest between YKGI and Kimly as well as Japan Foods. Visually it is manifested as the proportions of Blue, Orange, and Grey in a stacked bar that has been normalized to 100%. Thus the length of each bar is the same, and the length of each colour is approximately the same for YKGI, Kimly, and Japan Foods.

The comparison in this article is based on statistics from YKGI’s Preliminary Offer Document.

It seems to indicate that there is good potential for the company based on its current products and business model and by comparison with peers with a high degree of similarity. See Table 1 and Chart 1.

As long as YKGI’s portfolio of Singapore heartland food brands continues to serve affordable and consistently high-quality food, the potential exists for it to scale up to the next level.

Funds raised from the IPO will go towards business expansion here and overseas. YKGI is eyeing more market segments and brands, beefing up its supply chain, and forming joint ventures.

This article is contributed by ShareInvestor and Waterbrooks Editorial team.

See www.waterbrooks.com.sg for more information.

Notes on sources of information, statistics and assumptions

For original article, please visit: https://www.investor-one.com/editorial/22616-Yew-Kee-Duck-Rice-Attractive-Valuation-Delicious-Returns